DigitalOcean Stock Surges 12% in 2026 Amid SaaS Sector Collapse

February 2026 marks a turning point for the software industry. As the “SaaSpocalypse” unfolds, major SaaS giants like ServiceNow, Salesforce, and Adobe plummet. Yet one outlier defies the trend: DigitalOcean. Its stock climbs 12% year-to-date, while the IGV software ETF drops 22%. How does a developer cloud provider thrive when the rest of the sector crumbles?

Why DigitalOcean Stock Defies the SaaSpocalypse

The answer lies in structural advantages. Unlike seat-based SaaS models, DigitalOcean sells cloud infrastructure—compute, storage, and networking. AI adoption fuels demand for these resources, creating a flywheel effect. Here’s how it outperforms:

1. Infrastructure, Not Seat-Based SaaS

Traditional SaaS companies sell subscriptions tied to human users. AI agents reduce the need for human workers, directly threatening revenue. DigitalOcean’s infrastructure model thrives as AI scales. Every AI inference call, every generative AI model, requires cloud resources.

2. Consumption-Based Pricing

More data, more queries, more compute = more revenue. DigitalOcean’s usage-based model aligns with AI’s exponential growth. This contrasts sharply with per-seat models that stagnate as automation replaces human roles.

3. AI-Native Customer Growth

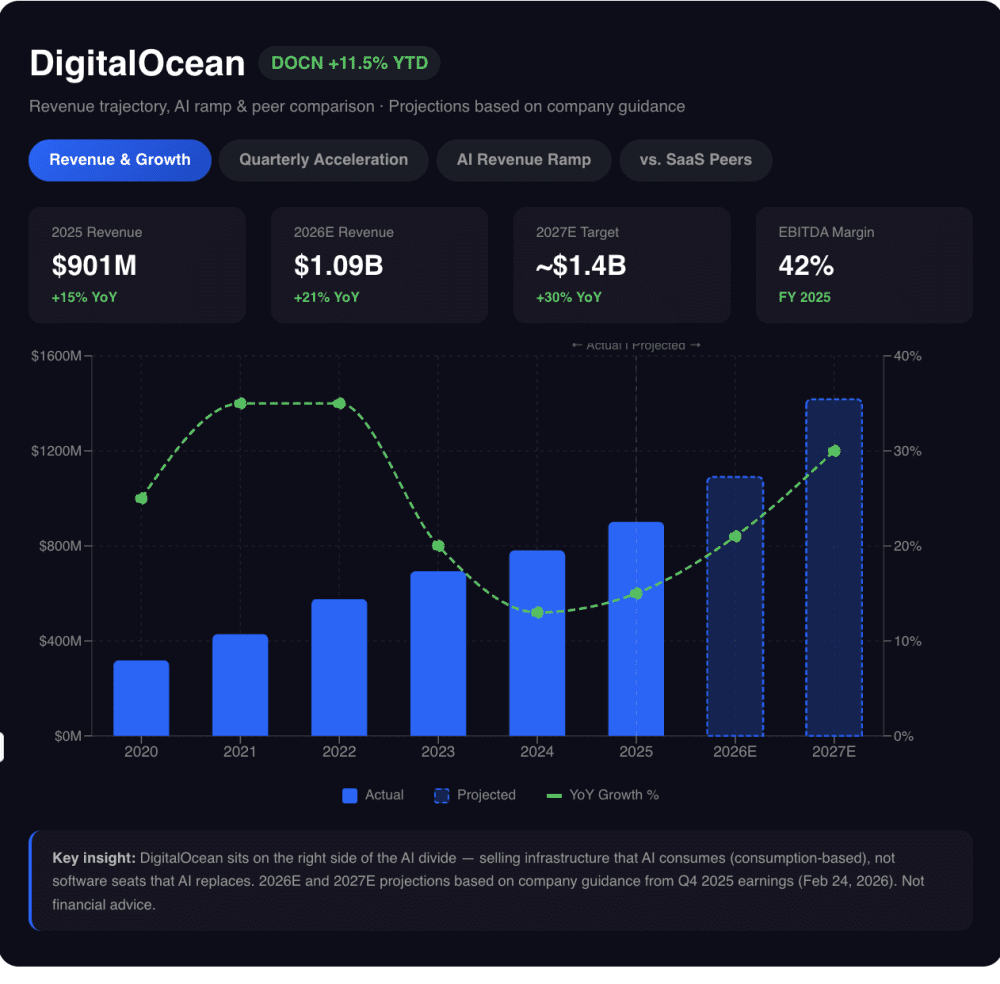

AI ARR contributes $120M (12% of total) in Q4 2025, growing 150% YoY. These customers span inference services and full-stack AI deployments, not just GPU rentals. Diversified revenue reduces reliance on top accounts.

4. Solved Customer Churn

Historically, startups migrated from DigitalOcean to AWS. Now, 62% of ARR comes from post-product-market-fit enterprises. Net dollar retention for $1M+ accounts hits 115%, with zero churn over 12 months.

5. Profitable Growth

2025 results show 42% EBITDA margins and $375M adjusted EBITDA. Free cash flow grows 19% YoY. With $254M cash and no debt maturities until 2030, DigitalOcean balances growth with financial discipline.

Contrasting the SaaS Sector

While DigitalOcean accelerates, competitors struggle:

- ServiceNow: Down 50% from highs despite 21% growth

- Adobe: P/E drops from 26x to 16x amid AI pricing shifts

- Workday: Faces pressure to abandon seat-based pricing

What This Means for Investors

DigitalOcean’s success highlights a broader trend: infrastructure wins in AI-driven markets. As AI adoption accelerates, companies with consumption-based models and diversified revenue streams will outperform. For investors, this means reevaluating SaaS valuations through the lens of AI readiness.