Smartphone Market Decline: What’s Next for Tech?

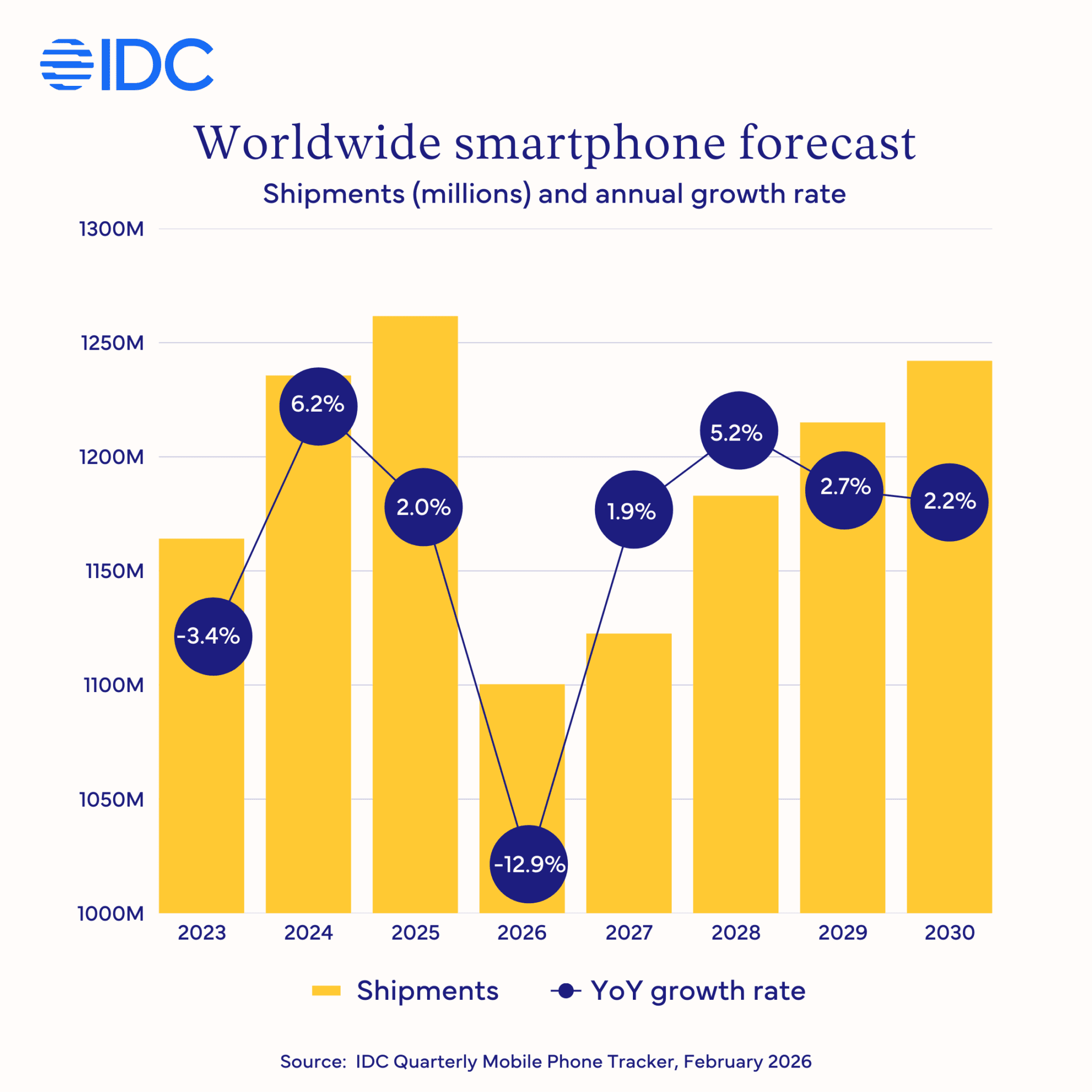

Global smartphone shipments are set for a dramatic drop in 2026. The International Data Corporation (IDC) forecasts a 12.9% year-on-year decline, bringing annual shipments to 1.1 billion units—the lowest level in over a decade. This crisis, driven by a memory shortage, is reshaping the industry for manufacturers and consumers alike.

The Memory Shortage Tsunami

Francisco Jeronimo, IDC vice president, calls the crisis a “tsunami-like shock” to the memory supply chain. Rising component costs are squeezing margins for low-end Android vendors, forcing them to raise prices. Meanwhile, Apple and Samsung are better positioned to weather the storm, potentially gaining market share as competitors struggle.

Key impacts include:

- Price shifts: Smartphone ASP (average selling price) will rise 14% to $523 in 2026.

- Market consolidation: Smaller vendors may exit, with sub-$100 smartphones becoming uneconomical.

- Supply chain ripple effects: Memory prices won’t return to pre-crisis levels until mid-2027.

Regional Impacts and Recovery Outlook

Markets with high low-end smartphone adoption will face the steepest declines. The Middle East and Africa are projected to drop 20.6%, while China and Asia Pacific (excluding Japan and China) will see 10.5% and 13.1% declines, respectively.

Recovery is expected to be gradual:

- 2027: A modest 2% rebound as the crisis stabilizes.

- 2028: A stronger 5.2% growth as memory prices stabilize.

What This Means for Consumers and Vendors

For consumers, the immediate effect is higher prices for entry-level devices. Low-end vendors may disappear, leaving fewer budget options. However, higher-end models could see improved quality as manufacturers shift focus.

Vendors must adapt quickly. As Nabila Popal, IDC senior director, explains: “This isn’t a temporary dip—it’s a structural reset. Companies that prioritize innovation and premium positioning will thrive.”