Introduction to Markov Chain Monte Carlo

While the world is captivated by the latest advancements in Large Language Models (LLMs), Markov Chain Monte Carlo (MCMC) remains a cornerstone of high-end quantitative finance and risk management. MCMC is a powerful tool for mapping out uncertainty when guessing isn’t enough.

Understanding Markov Chain Monte Carlo

A Markov Chain is a stochastic process where the next state depends entirely on its current state, not on the sequence of events that preceded it. Meanwhile, a Monte Carlo method relies on repeated random sampling to obtain numerical results.

The Problem MCMC Solves

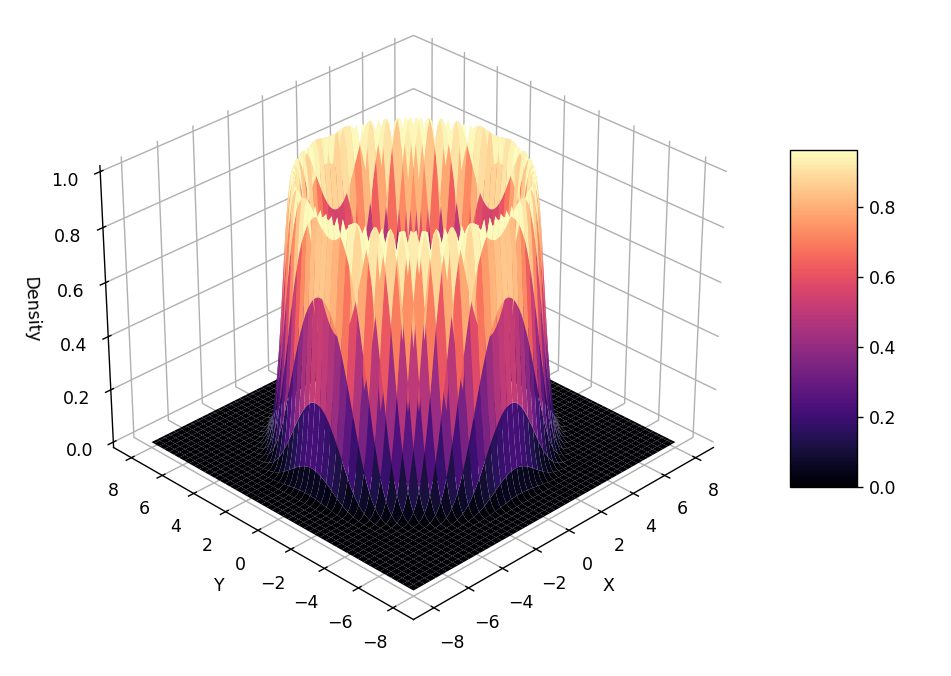

Suppose we want to sample variables from a probability distribution for which we know the density formula. For instance, the standard normal distribution. To achieve this, we start with the formula for the unnormalized density of the normal distribution: p(x) = e^(-x^2/2).

This function returns a density for a given x instead of a probability. To get a probability, we need to normalize our density function by a constant, so the total area under the curve integrates to 1.

Markov Processes and Transition Probabilities

A Markov process is uniquely defined by its transition probabilities P(x → x’). For example, in a system with 4 states, the probability of going from any state x to x’ is given by the entry i → j in the transition matrix.

Stationary Distribution

A properly constructed Markov process reaches a state of equilibrium as the number of steps t approaches infinity. This state is known as global balance, and the distribution at this point is called the stationary distribution.

The existence of such a state is the foundation of every MCMC method. When sampling a target distribution using a stochastic process, we aren’t asking ‘Where to next?’ but rather ‘Where do we end up eventually?’.

Conclusion and Next Steps

In conclusion, Markov Chain Monte Carlo is a powerful tool for quantitative finance and risk management. By understanding Markov Chains and Monte Carlo methods, we can effectively estimate probabilities and make informed decisions.

For further learning, consider exploring the Metropolis-Hastings algorithm, a foundational algorithm in MCMC frameworks.

Frequently Asked Questions

- What is Markov Chain Monte Carlo used for? MCMC is used for mapping out uncertainty in quantitative finance and risk management.

- How does MCMC work? MCMC works by using a stochastic process to sample from a target distribution.

- What is the stationary distribution in MCMC? The stationary distribution is the distribution at which the Markov process reaches a state of equilibrium.

- What is the Metropolis-Hastings algorithm? The Metropolis-Hastings algorithm is a foundational algorithm in MCMC frameworks.

- Why is MCMC important? MCMC is important because it allows us to effectively estimate probabilities and make informed decisions in quantitative finance and risk management.